FSA- and HSA-eligible items: 30+ unexpected products that can save you money in 2026

Most people with an FSA or HSA are leaving money on the table. This guide covers 30+ eligible items you can buy with pre-tax dollars in 2026, from massage guns and fertility tests to light therapy masks and dental aligners, plus a year-end checklist so you never forfeit your balance again.

The average American spends about $13,500 on healthcare every year, and most of them are leaving money on the table. Flexible spending accounts (FSAs) and health savings accounts (HSAs) let employees pay for hundreds of eligible products and services with pre-tax dollars, which means real savings on costs they're already paying. Most people know these accounts cover copays and prescriptions. Far fewer know they also cover light therapy masks, fertility tests, massage guns, and dozens of other everyday items.

That's good news for employees, and for employers too. With thousands of products available for purchase via HSA or FSA, these tax-advantaged accounts aren't just a boon for the people using them. They can offer significant cost savings to the employers offering them, as well. If your company isn't offering these accounts yet, you might be able to make your team's lives easier (and healthier) without breaking your budget.

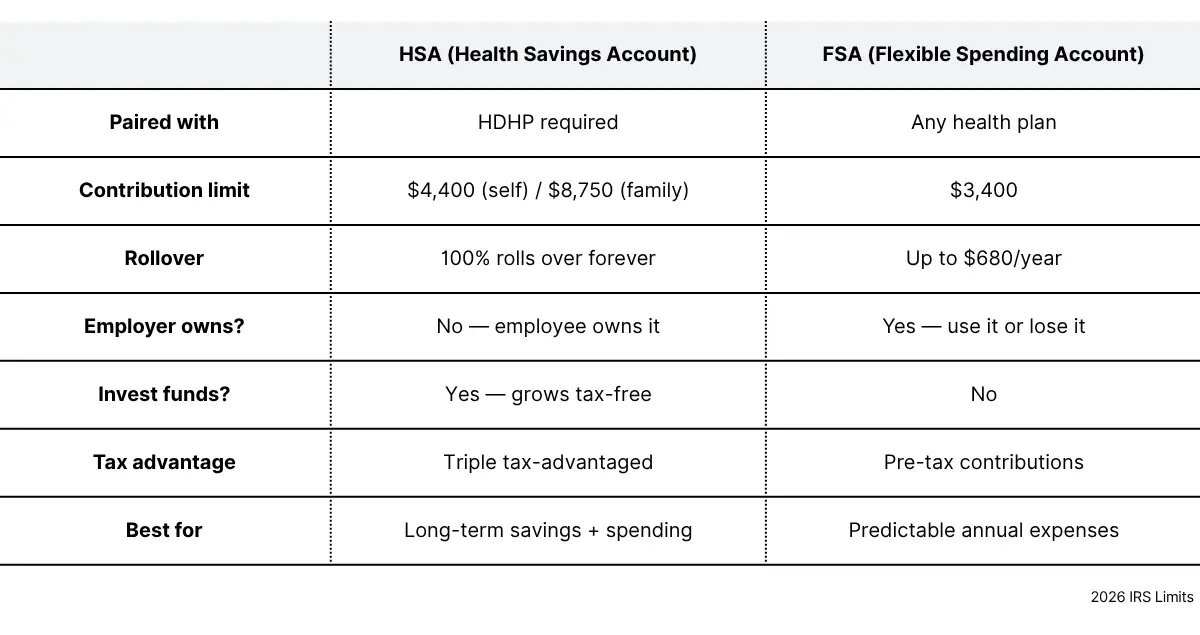

FSA vs. HSA: What's the difference for eligible items?

The good news: FSA and HSA eligible item lists are nearly identical. Most products that qualify for one qualify for the other. The key differences are in the account mechanics: FSA funds are use-it-or-lose-it each plan year (with limited rollover), while HSA balances roll forward indefinitely and can be invested. If you have an HSA, you may also be eligible for a Limited-Purpose FSA (LP-FSA) to cover dental and vision costs.

The accounts are designed for the obvious stuff: doctor visits, prescriptions, contact lenses. But there are thousands of qualifying products that never make it into the open enrollment presentation. This list covers 24 of the best ones, organized by category, so you actually know what to look for.

Pro tip: Amazon has a dedicated FSA/HSA store with a filter to show only eligible products. Target and Walmart do too.

What are the best FSA- and HSA-eligible items?

FSA and HSA eligibility covers a broad spectrum of health and wellness products. There are thousands (seriously, thousands!) of products available for purchase through these accounts, and some of them may surprise you. Let’s dive into the best — and most unexpected items — to buy with your HSA and FSA.

Tech and health devices

A lot of the most surprising FSA-eligible items fall into this category — products that live at the intersection of consumer wellness tech and genuine medical utility.

- Light therapy face masks: The red-light and blue-light masks popular on social media (including the Dr. Dennis Gross SpectraLite FaceWare Pro) are FSA-eligible when used to treat conditions like acne or skin inflammation. The key is that they must be used for a specific medical purpose, not general skincare.

- TENS therapy devices: Transcutaneous electrical nerve stimulation (TENS) units use low-voltage electrical current to relieve pain. Handheld devices like the Compex Sport or Omron Max Power Relief are FSA-eligible and widely available.

- Massage guns: Devices like the Theragun are FSA-eligible when used to address a diagnosed condition like muscle pain or injury recovery. Keep your receipts.

- Blood pressure monitors: At-home cuffs from Omron, Withings, and others are fully FSA-eligible with no additional documentation required.

- Continuous glucose monitors (CGMs): Devices like Dexcom and Libre are FSA-eligible for people managing diabetes, and increasingly accessible without a prescription depending on the model.

- Sleep health trackers and CPAP supplies: CPAP machines, masks, and accessories are fully FSA-eligible. Some sleep trackers qualify as well, though you may need a letter of medical necessity (LMN) depending on your plan administrator.

Women's health and reproductive care

Thanks to the CARES Act, passed in 2020, a wide range of women's health products became FSA-eligible for the first time. This is a category worth highlighting for HR leaders, especially during open enrollment.

- Menstrual products: Tampons, pads, liners, menstrual cups, menstrual discs, and period underwear are all FSA-eligible. This changed in 2020 and is now permanent.

- Hot flash and menstrual relief devices: Wearable relief devices like Embr Wave (for hot flashes) and Livia (for menstrual cramps) are eligible.

- At-home hormone tests: Tests for ovulation, perimenopause, and fertility hormone levels qualify. These can be especially valuable for employees trying to conceive or navigating reproductive health decisions.

- Pregnancy tests: Fully eligible — useful to call out explicitly since employees sometimes assume they're not covered.

- Prenatal vitamins: Unlike most vitamins, prenatal vitamins are FSA-eligible because they're used to support a specific health condition (pregnancy).

- Postpartum recovery items: C-section recovery bands, postpartum pain relief sprays, nipple cream, breast pump accessories, and more are all covered. Breast pumps themselves are eligible too.

Oral and dental care

Dental expenses are a major driver of out-of-pocket healthcare spending. A handful of products go further than most people realize.

- At-home dental aligners: Services like Byte and Candid, which offer remote orthodontic treatment, are FSA-eligible. This is a significant cost item that employees with FSA funds can put to work.

- Oral light therapy devices: Devices that use light technology to promote gum health and reduce bacteria are eligible.

- Electric toothbrushes: Standard electric toothbrushes are NOT FSA-eligible on their own. However, if your dentist writes a letter of medical necessity citing gum disease or a specific oral health condition, reimbursement may be possible through your plan administrator.

- Medicated lip balm: Lip balms with SPF 15 or higher, or those formulated for a medical condition like cold sores, are eligible. Standard moisturizing balm is not.

- Mouthguards for bruxism: Night guards prescribed or recommended for teeth grinding are FSA-eligible.

Skincare and beauty (the FSA-eligible ones)

Americans spend an average of $85 per month on skincare. A portion of that spending may be FSA-eligible, but only when the product has a specific medical function.

- Sunscreen (SPF 15 or higher): Broad-spectrum sunscreen with SPF 15 or higher is FSA-eligible. This includes popular products from EltaMD, Supergoop, and CeraVe. Sunscreen-infused makeup is generally not eligible.

- Acne treatment products: Over-the-counter acne treatments, including patches like Mighty Patch, benzoyl peroxide washes, and salicylic acid treatments, are eligible without a prescription.

- Light therapy acne devices: LED face masks designed specifically for acne treatment are eligible. Dual-purpose beauty devices may require an LMN.

- Medicated shampoos: Shampoos formulated to treat dandruff, psoriasis, or seborrheic dermatitis (think Head & Shoulders, Nizoral) are FSA-eligible. Regular shampoo is not.

Everyday medicine cabinet staples

The CARES Act also removed the prescription requirement for over-the-counter medications as of 2020. This opened up a wide range of everyday items that many employees still don't know they can purchase with FSA funds.

- Pain relievers: Ibuprofen, acetaminophen, naproxen — all FSA-eligible without a prescription.

- Allergy medications: Antihistamines, decongestants, and nasal sprays like Claritin, Zyrtec, and Flonase are all eligible.

- Antacids and digestive aids: Tums, Pepto, Zofran ODT, Gas-X — eligible.

- Cold and flu medicine: NyQuil, DayQuil, Theraflu, Mucinex — all eligible.

- First-aid kits: Pre-assembled kits and individual supplies (bandages, antiseptic wipes, gauze) are eligible.

- Skin repair sprays and wound care: Products like Neosporin, hydrocortisone cream, and antiseptic sprays are eligible.

- Specialty baby wipes: Standard baby wipes are NOT eligible, but medicated or specialty wipes (like Boogie Wipes for nasal congestion) are.

Family and parenting

Parenting is expensive. FSAs and dependent care FSAs (DC-FSAs) can offset a meaningful amount of that cost.

- Smart baby monitors: Standard audio-only monitors are not FSA-eligible. Video monitors generally aren't either, unless they include medical-grade health tracking features.

- Baby breathing and oxygen monitors: Devices that track infant breathing patterns and oxygen levels, like the Owlet Dream Sock, are FSA-eligible.

- Bandages, thermometers, and kid-specific OTC meds: Children's Tylenol, Motrin, Benadryl, digital thermometers, and basic first-aid supplies are all eligible.

A note on dependent care FSAs (DC-FSAs): Daycare, preschool, summer day camps, and after-school care for children under 13 are eligible under a dependent care FSA, not a standard healthcare FSA. For 2026, the DC-FSA contribution limit increased to $7,500 (up from $5,000), thanks to the One Big Beautiful Bill Act. This is a meaningful benefit for working parents that is frequently undersold during open enrollment.

What requires a letter of medical necessity (LMN)?

Some products sit in a gray zone: they have legitimate medical uses but also non-medical applications, so FSA administrators require documentation before reimbursing them. A letter of medical necessity (LMN) is a written statement from a licensed healthcare provider confirming that a specific product or service is medically necessary for a diagnosed condition.

Products that commonly require an LMN include:

- Ergonomic chairs and standing desks: May qualify when prescribed to address a diagnosed back condition.

- Gym memberships and fitness equipment: Generally not eligible on their own, but may qualify with an LMN if prescribed to treat obesity, diabetes, or a specific chronic condition.

- Air purifiers and humidifiers: May qualify for diagnosed respiratory conditions like asthma or severe allergies.

- Weighted blankets: Sometimes approved for anxiety disorders or sensory processing conditions.

- Wigs: May qualify for medically-caused hair loss (chemotherapy, alopecia).

If you're unsure whether something qualifies, check with your FSA administrator before purchasing. Keep itemized receipts (not just credit card statements) for anything you plan to submit for reimbursement.

Where to shop for FSA-eligible items

You can use your FSA debit card or pay out of pocket and submit for reimbursement at most major retailers:

- Amazon: Amazon's FSA/HSA Store lets you filter search results to show only eligible products.

- CVS, Walgreens, Rite Aid: Most pharmacy chains have FSA-eligible sections in store and online, with automatic identification at checkout.

- Target and Walmart: Both have dedicated FSA/HSA sections on their websites.

- FSA Store and HSA Store: Dedicated retailers that sell only FSA/HSA-eligible products, which eliminates the guesswork.

If your plan issues an FSA debit card, the card will often auto-approve eligible items at IIAS-certified retailers. For non-certified retailers or ambiguous items, you'll pay out of pocket and submit for reimbursement with an itemized receipt.

2026 FSA and HSA contribution limits

Here's a quick reference for 2026 limits, updated based on IRS Revenue Procedure 2025-32 and the One Big Beautiful Bill Act:

- Healthcare FSA: $3,400 maximum contribution (up from $3,300 in 2025)

- FSA rollover limit: $680 maximum carryover for plans with a rollover provision (up from $660)

- Dependent Care FSA (DC-FSA): $7,500 maximum contribution (up from $5,000 — a major increase)

- HSA (self-only coverage): $4,400 maximum contribution

- HSA (family coverage): $8,750 maximum contribution

How to use your HSA as a retirement savings tool

If you have an HSA, you don't have to spend it right away — and in many cases, you shouldn't. A strategy called HSA shoeboxing lets you turn your account into a long-term savings vehicle. Instead of reimbursing yourself for healthcare costs immediately, you pay out of pocket, save your receipts (the "shoebox"), and leave your HSA funds in the account to grow. Because HSAs offer investment options, your balance can compound tax-free year after year.

Here's how withdrawals work:

- Before age 65: If you withdraw funds for anything other than qualified medical expenses, the IRS treats it as regular income and adds a 20% penalty. That makes shoeboxing less about short-term spending and more about growing a nest egg for later.

- After age 65: The 20% penalty disappears. You can withdraw funds for any purpose. If it's for medical expenses, it remains tax-free. If it's for non-medical expenses, it's simply taxed as income, just like pulling from a 401(k) or IRA.

Because contributions are tax-free, earnings grow tax-free, and qualified withdrawals are tax-free, HSAs are often called triple tax-advantaged accounts. With shoeboxing, you maximize all three, letting your money grow while keeping the option to reimburse yourself later using those saved receipts.

Frequently asked questions

What is FSA eligible?

An FSA-eligible item is any product or service the IRS classifies as a qualified medical expense under Section 213(d) of the tax code. This includes items used to diagnose, treat, prevent, or cure a specific medical condition. Common examples include prescription medications, OTC medicines (no prescription required since 2020), medical devices, menstrual products, and mental health services. General wellness spending, like gym memberships or most vitamins, is not eligible without medical documentation.

What is the difference between FSA and HSA eligible items?

For products, the eligible item lists are nearly identical. If something is FSA-eligible, it's almost always HSA-eligible too. The primary difference is in the accounts themselves: FSA funds must typically be used within the plan year (with limited rollover), while HSA funds roll over indefinitely. HSAs also allow you to invest unused funds and can be used to pay Medicare and COBRA premiums under specific conditions, while FSAs cannot.

Can I use my FSA on Amazon?

Yes. Amazon has a dedicated FSA and HSA store that lets you filter products to show only eligible items. You can pay directly with your FSA debit card, and Amazon will automatically identify eligible items at checkout. Look for the 'FSA or HSA eligible' badge on product listing pages.

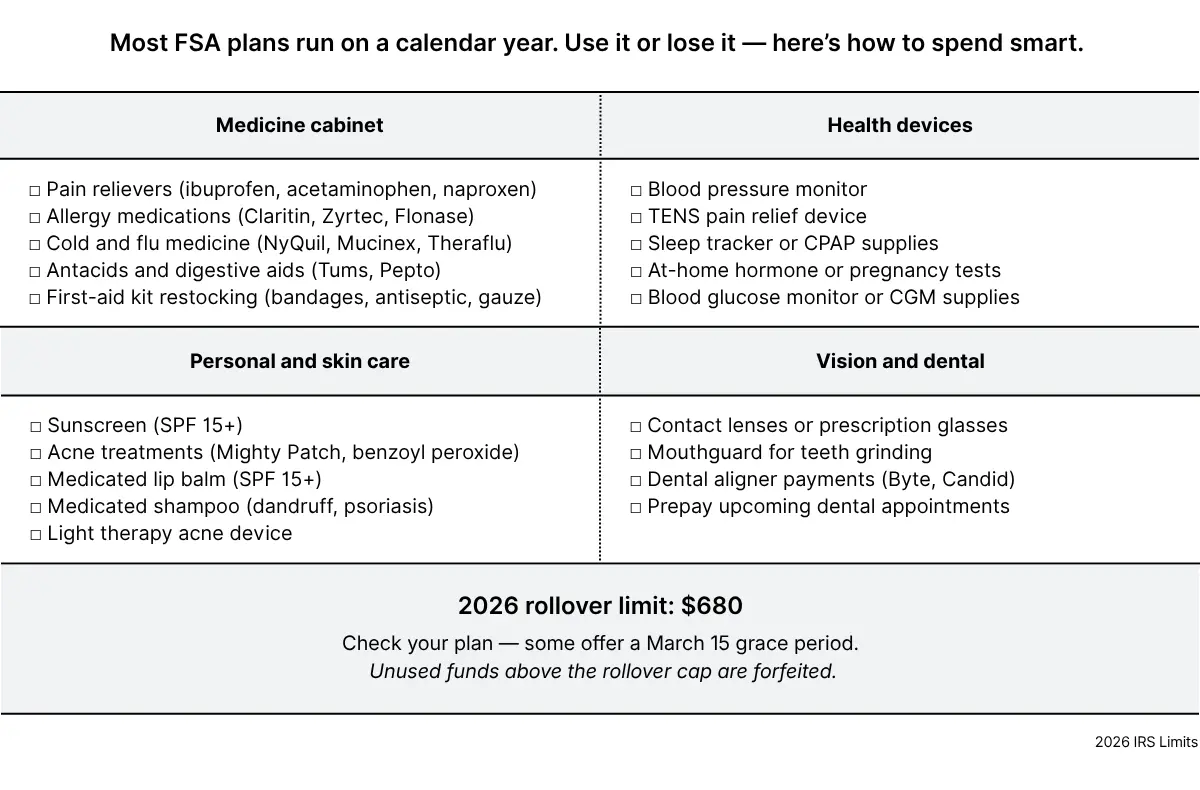

What FSA items can I buy at the end of the year to use up my balance?

If you have leftover FSA funds as the year-end approaches, consider stocking up on: OTC medications (pain relievers, allergy meds, cold medicine), contact lenses or glasses, sunscreen, acne treatments, menstrual products, a blood pressure monitor, a first-aid kit, or dental care items.

You can also prepay for upcoming medical appointments or procedures if they fall within your plan's grace period. Check your specific plan rules — some offer a March 15 grace period or a $680 rollover for 2026.

Are sunscreen and skincare products FSA eligible?

Sunscreen with SPF 15 or higher is FSA-eligible. Some medicated skincare products, like acne treatments, medicated shampoos, and prescription topicals, are also eligible. General moisturizers, anti-aging products, and non-medicated cosmetics are not eligible, even if they have some health benefit.

What items require a letter of medical necessity for FSA reimbursement?

Items with both medical and non-medical uses may require an LMN: a written statement from a licensed provider explaining that the item is necessary to treat a specific diagnosed condition. Common examples include ergonomic equipment, air purifiers, gym memberships, and certain fitness devices. Check with your FSA administrator before purchasing, and save all itemized receipts.

A note for HR leaders

If you're an HR leader evaluating whether to add an FSA or HSA to your benefits package or wondering how to better communicate FSA value to employees, Nava's benefits advisors can help. FSAs cost most employers about $5 per employee per month to administer and generate payroll tax savings that often exceed that cost. They're one of the highest-ROI, lowest-effort benefits available, and they're frequently undersold during open enrollment.

Note: FSA eligibility is determined by the IRS and interpreted by individual plan administrators. Some items may require additional documentation. Always confirm eligibility with your plan administrator before purchasing. Contribution limits reflect 2026 IRS guidance (Rev. Proc. 2025-32).