HDHP vs. PPO: everything you wish you knew before picking a health plan

Choosing between an HDHP and a PPO is one of the most important financial decisions employees make each year, yet most people do it without the full picture. This guide breaks down how high deductible health insurance actually works, who it's a smart fit for, and where it can backfire, including real talk on costs, HSA benefits, and what families with frequent care needs should watch out for. Whether you're an HR leader building your benefits strategy or an employee staring down open enrollment, here's what you need to make the right call.

Every fall, open enrollment arrives with a stack of plan options, dense benefit summaries, and a deadline that feels closer than it is. If you've ever stared at the words "high deductible health plan" and quietly wondered what they actually mean for you, you're not alone.

High deductible health plans have a bit of a reputation problem. The name alone puts people off. But the full picture is more nuanced than it first appears, and for many people and organizations, an HDHP can genuinely work in everyone's favor.

This guide breaks it all down, without the jargon.

What is a high deductible health plan?

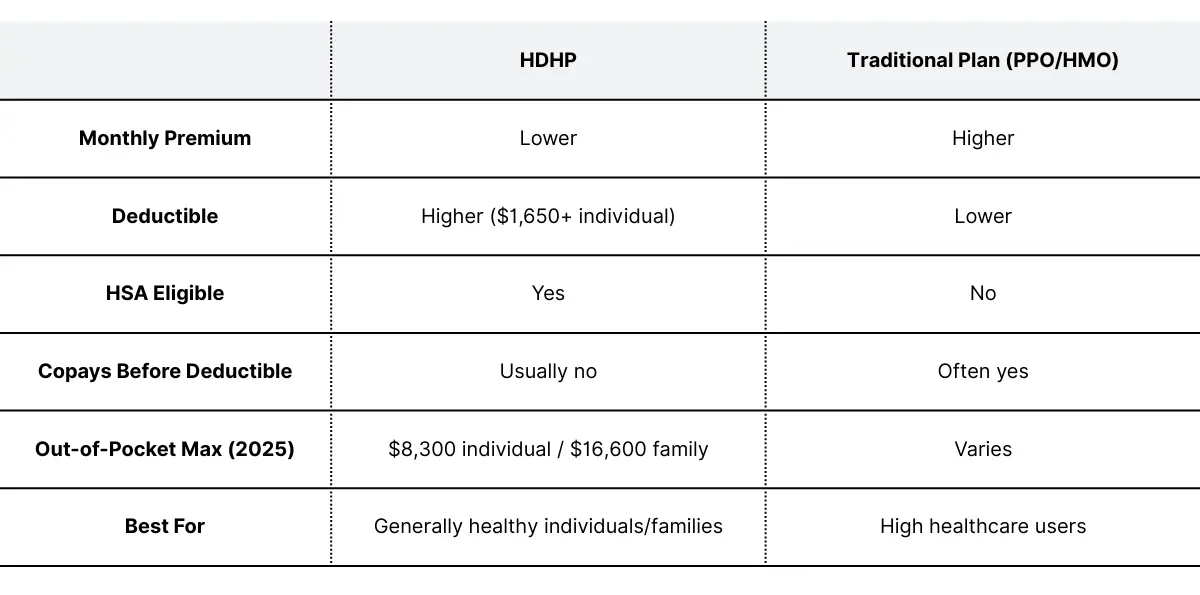

A high deductible health plan, or HDHP, is a health insurance plan with a higher annual deductible than traditional plans, paired with a lower monthly premium. In 2026, the IRS defines an HDHP as any plan with a deductible of at least $1,700 for individuals or $3,400 for families.

The key tradeoff: you pay less each month, but you pay more out-of-pocket before your insurance kicks in for most services. Preventive care (like annual physicals and vaccines) is typically covered at no cost from day one.

HDHPs also come with a major perk that traditional plans don't: eligibility for a Health Savings Account, or HSA. More on that in a moment.

Here's how high deductible health insurance compares to a traditional plan at a glance:

HDHP vs. PPO: What's the difference?

One of the most common questions during open enrollment is how a high deductible health plan vs. a PPO actually stacks up. Both can give you access to a wide network of doctors, but the cost structure is very different.

With a PPO, you typically pay higher monthly premiums but lower costs when you actually use care, often through copays before your deductible.

With an HDHP, you pay lower premiums but take on more out-of-pocket costs upfront until your deductible is met.

For healthy individuals and families who don't use a lot of care, the math often favors the HDHP. For people who see specialists regularly or have ongoing prescriptions, the PPO may come out ahead. The only way to know for sure is to model out your likely annual spend under each plan.

The real pros of an HDHP

The most obvious benefit is the lower monthly premium, but that's just the beginning.

Lower monthly costs

You pay less in premiums every month, which means more money stays in your paycheck. For employees who rarely use healthcare, this can add up to real savings over the course of a year.

Access to an HSA

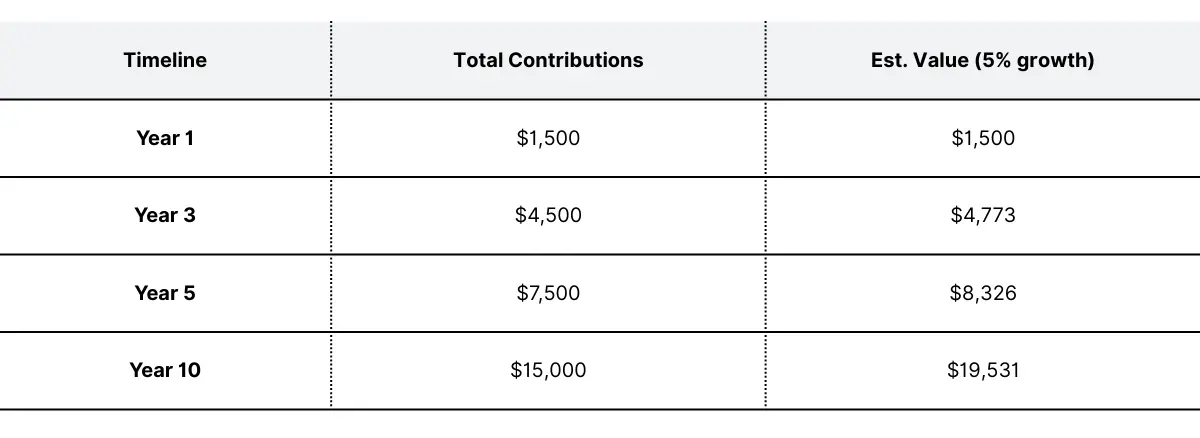

The HDHP with HSA combination is arguably one of the most powerful tools in the benefits lineup. With an HSA, you can contribute pre-tax dollars, your money grows tax-free, and withdrawals for qualified medical expenses are also tax-free. That's a triple-tax advantage no other savings account offers.

Unlike a Flexible Spending Account (FSA), your HSA balance rolls over every year and never expires. You can invest it, and after age 65, you can withdraw it for any purpose penalty-free, similar to a traditional IRA.

Here's what consistent HSA contributions could look like over time:

Many employers also contribute to employee HSAs as part of their benefits package, adding even more value to the equation.

Encourages cost-aware healthcare decisions

When people pay more out-of-pocket, they tend to engage more with healthcare costs, whether comparing costs, using in-network providers, or asking whether a test or procedure it actually necessary. Research suggests this can lead to more deliberate spending decisions over time.

The real cons of HDHPs

The right plan depends on your situation, and there are real tradeoffs to understand before deciding.

High out-of-pocket exposure before the deductible

The biggest downside to having a high deductible is straightforward: until you meet it, most services, including specialist visits, lab work, and prescriptions, are paid out of pocket. For someone with an unexpected illness or injury early in the plan year, this can be a significant financial burden.

Can discourage necessary care

Studies show that when costs feel high upfront, some people delay or skip care they actually need. This is one of the most legitimate criticisms of HDHPs, and it's worth taking seriously when evaluating whether this plan type is right for your situation.

Harder to navigate for families and chronic conditions

For a family with children, the question of PPO or HDHP deserves careful thought. Kids tend to need more frequent care, from sick visits to physicals to the occasional urgent care trip, and those costs add up before your deductible kicks in.

The same logic applies if you're managing ongoing prescriptions or regular specialist visits. The premium savings may not outweigh what you'll spend before the deductible resets each plan year.

Who a high deductible health plan works best for

The right plan depends on your health situation, financial cushion, and how you use care throughout the year.

HDHPs might be a great fit for:

- Generally healthy individuals or couples who rarely see a doctor beyond annual check-ups

- People who want to build long-term savings through an HDHP + HSA combo

- Employees with an emergency fund or HSA balance to cover the deductible if needed

- Those who are younger and earlier in their careers, looking to maximize take-home pay

HDHPs are worth running the numbers for:

- Families with young children who tend to use care more frequently

- Anyone managing a chronic condition, ongoing prescriptions, or planned procedures

- People who may not have the cushion to cover a high deductible in an unexpected medical situation

The bottom line: don't choose a plan based on the premium alone. Model out your likely annual costs under each option.

How to make the most of an HDHP

If you've landed on a high deductible health plan, here's how to use it strategically:

- Max out your HSA contributions early in the year if you can. The 2026 contribution limits are $4,400 for individuals and $8,750 for families.

- Take full advantage of preventive care. Annual physicals, screenings, and vaccines are typically covered at no cost, even before your deductible.

- Build a deductible cushion. Aim to keep at least your annual deductible amount accessible, either in your HSA or emergency fund.

- Invest your HSA balance. Once you've built a comfortable cash buffer, most HSA providers let you invest the remainder in mutual funds or ETFs.

- Compare costs before scheduling care. Use your insurer's cost estimator tool to find lower-cost in-network providers for non-urgent services.

How to make the right call: decision support tools explained

Choosing between an HDHP and a traditional plan used to mean squinting at summary of benefits documents and hoping you guessed right. Decision support tools have changed that, giving both employees and HR teams a smarter, more personalized way to navigate open enrollment.

For employees: use the decision support tools available to you

If your employer offers a decision support tool during open enrollment, use it. These tools are designed to take the guesswork out of plan selection by factoring in your specific situation, not just the headline numbers on the benefits page.

A good decision support tool will ask about your current prescriptions, any planned procedures or specialist visits, and your preferred doctors. It then models out your likely annual costs under each plan option so you can compare apples to apples. For many people, this kind of personalized analysis is the difference between picking a plan that saves money and accidentally choosing one that costs significantly more.

Think of it less like a benefits quiz and more like a financial calculator built specifically for your healthcare decisions.

For HR leaders: invest in a decision support tool

One of the biggest mistakes organizations make is offering a high deductible health plan without giving employees the tools to evaluate whether it's right for them. A decision support tool bridges that gap.

With the right tool, employees can input their prescriptions, anticipated procedures, and doctor preferences to get a personalized plan recommendation. This reduces confusion during open enrollment, minimizes post-enrollment regret, and cuts down on the volume of HR questions you'd otherwise field.

Nava's decision support tool guides employees through exactly this process, helping them weigh real costs and make confident decisions. It also confirms doctor network coverage before employees enroll, one of the most common sources of frustration.

The bigger picture

When high deductible health insurance plans are paired with meaningful employer HSA contributions and the right decision support tools, they can genuinely work well for both employees and organizations. Employees gain flexibility, long-term savings potential, and lower monthly costs. Employers can reinvest the premium savings into richer HSA contributions or other benefits that matter to their teams.

The key is giving employees what they need to make an informed choice, rather than leaving them to figure it out on their own.

Your next step

Before open enrollment closes, take 10 minutes to run the numbers on your options. If your employer offers a decision support tool, start there. If not, ask your HR team whether one is available or coming soon.

Picking the right plan for your situation is one of the highest-ROI decisions you'll make this year. It's worth the time.

.webp)

.webp)